When starting a small business, there are several critical decisions that can shape your company’s future. One of the most significant decisions you will have to make is your classification; this will determine how you pay taxes and report earnings. Will you classify your business as an LLC? Or are you working with a partner — and consequently choosing the partnership classification? Single employee businesses are most often classified as sole proprietorships.

But what exactly does this mean for your business, and what are the benefits of a sole proprietorship over, say, a single-person LLC? This article addresses some of the minutiae of taxes for small businesses alongside the implications, benefits, and advantages of running a sole proprietorship. Use the links below to navigate the article.

A sole proprietorship is the default business classification for any single-person business or contractor engaging in business activities. Under a sole proprietorship, there is no distinction between the business owner as an individual and the company itself, as far as the IRS is concerned. Many business owners who maintain single-employee businesses choose to keep this classification as it makes business taxes much more straightforward.

Sole proprietorships are considered a “pass-through entity,” meaning that revenue “passes through” to the owner. Because of this, sole proprietorships are exempt from certain business taxes that larger corporations have to contend with.

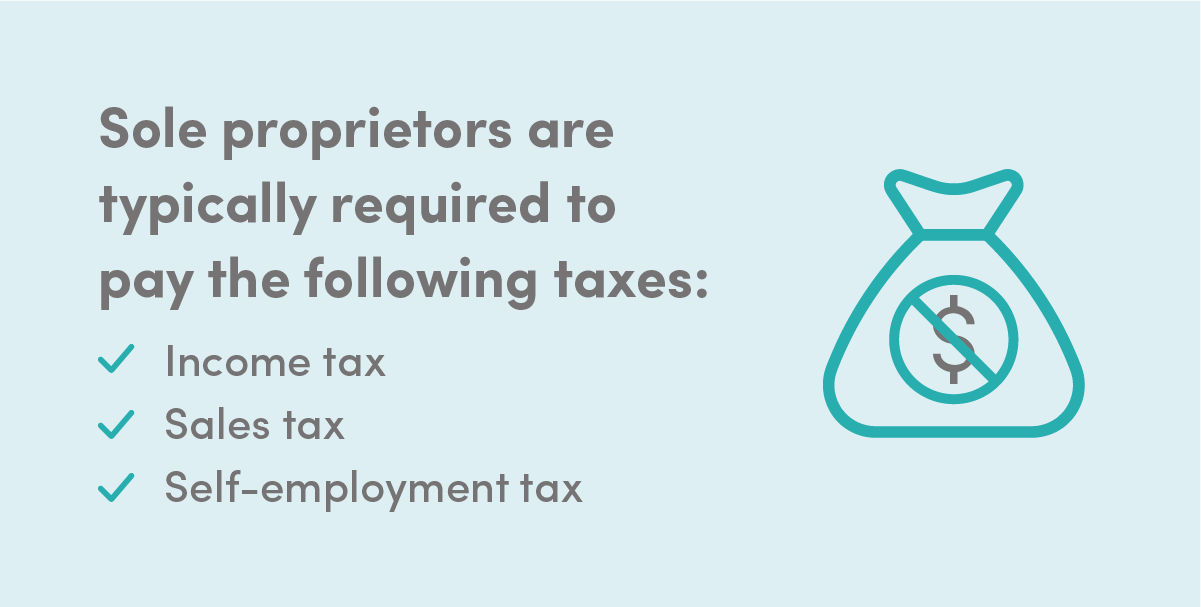

Sole proprietors have to pay income tax at the federal and, if applicable, the state level. Also, sole proprietors must contend with sales tax (if applicable) and self-employment tax. Self-employment tax goes towards Social Security and Medicare — usually paid for by your employer, but in this case, you are the employer.

Finally, sole proprietors have to contend with federal and state estimated tax. In a nutshell, estimated tax is the amount you estimate you will owe for employment and income taxes at the end of the year. Estimated tax is paid every quarter, on the 15th of January, April, June, and September. We will further examine estimated tax later in the article.

Related Reading: Advantages of Running a Small Business

Sole proprietorship tax returns are much more closely intertwined with personal tax returns compared to corporation taxes. However, there are still several unique steps that sole proprietors have to complete come tax time. Chief among these steps is listing your profit and loss statement on a Schedule C alongside form 1040.

Schedule C (Profit or Loss from a Business) consists of five parts:

The first part of Schedule C records your business’s income for the relevant tax year. On this item, you must report:

You will use these items to calculate your total gross income.

Because there are a myriad of possible expense categories, there are many different items in Section II, even though many sole proprietors will only use a fraction of these items. They include:

Although this list is extensive, a sole proprietorship may have qualifying business expenses that don’t fall neatly into any of these categories. The miscellaneous spend will need to be reported in Section V (other expenses) and subsequently added to Section II’s total spend.

After these expenses are added up, you subtract the total amount from section I. The resulting figure is known as tentative profit or loss.

If you use any part of your home for business activities, you need to report it in this section. There are two ways to do this: either attaching Form 8829, Expenses for Business Use of Your Home or using the Simplified Method worksheet. The purpose of this is to put a monetary value on any personal space used for business activities. The resulting figure is then subtracted from your tentative profit or loss to get your net profit or a net loss. If you made a net loss in the relevant tax year, your work might not be done; you may have to attach Form 6198, At-Risk Limitations.

Sections I and II together paint a clear picture of any sole proprietorship’s cashflow health to the IRS. They comprise the mandatory part of Schedule C that every single sole proprietorship needs to complete. Some sole proprietorships may be exempt from some or all of the remaining sections, depending on applicability.

This section needs to be completed by any sole proprietorships that operate with an inventory. The cost of goods sold is simply the measure of how much it costs to produce products, including direct material or labor expenses.

When filling out Section III, you must disclose the method you use to value your business’s closing inventory. Also, you will need to list:

You will then subtract the value of your year-end inventory from this amount to find your total cost of goods sold.

If you are claiming vehicle expenses — and are not required to file Form 4562 — you will need to fill out Section IV. Section IV asks for the date you started using your vehicle for business purposes, the number of miles you drove your vehicle in the past year for business and commuting, whether you used your vehicle for personal reasons, and whether you have written evidence to support your deductions.

In Section V, you must itemize each business expense that is not accounted for in the previous four sections. Most sole proprietors do not need to fill out Section V.

There are a plethora of tax benefits for sole proprietors. Some of the more straightforward ones, such as pass-through designation, are automatically applied to your return. There are several more complicated or obscure benefits hidden in tax laws, however. Outsourcing your accounting and bookkeeping to professionals is the most efficient and most cost-effective way to save your business money come tax time. The small business accountants at FinancePal have helped thousands of sole proprietorships with their financials on a convenient subscription basis. FinancePal also has a team of small business tax preparation experts who are able to find the best tax benefits and savings for your sole proprietorship. Schedule a consultation today!

Jacob Dayan is a true Chicagoan, born and raised in the Windy City. After starting his career as a financial analyst in New York City, Jacob returned to Chicago and co-founded FinancePal in 2015. He graduated Magna Cum Laude from Mitchell Hamline School of Law, and is a licensed attorney in Illinois.

Jacob has crafted articles covering a variety of tax and finance topics, including resolution strategy, financial planning, and more. He has been featured in an array of publications, including Accounting Web, Yahoo, and Business2Community.

Nick Charveron is a licensed tax practitioner, Co-Founder & Partner of Community Tax, LLC. His Enrolled Agent designation is the highest tax credential offered by the U.S Department of Treasury, providing unrestricted practice rights before the IRS.

Read More

Jason Gabbard is a lawyer and the founder of JUSTLAW.

Andrew is an experienced CPA and has extensive executive leadership experience.

Contact us today to learn more about your free trial!

By entering your phone number and clicking the "Get Custom Quote" button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.

By entering your phone number and clicking the “Get Started” button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.