Because healthcare is so closely tied to politics, the laws and circumstances surrounding it are prone to rapid change. Sound accounting, bookkeeping, and financial management are imperative for any hospital or healthcare service to navigate the ever-changing landscape of the healthcare industry.

In 2010, the Affordable Care Act (ACA), combined with changes in Medicare coding and the adoption of electronic medical records changed the healthcare playing field once more. As with all changes, this threatened hospitals and healthcare services who didn’t have sound accounting with fees, fines, and even criminal charges.

In the healthcare industry, shoddy accounting brings a plethora of risks that can hurt profitability. That is why proper, GAAP-compliant accounting and bookkeeping are integral to the financial health and performance of any hospital or healthcare service.

In the healthcare industry, there are two methods of reporting on the Profit and Loss Statement (PnL Statement) and the balance sheet: the accrual method and the cash method.

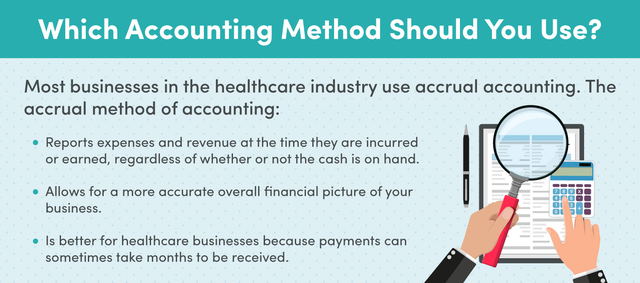

The accrual method of accounting reports expenses and revenue at the time they are incurred or earned, regardless of whether or not the cash is on hand. The biggest advantage of the accrual method is accuracy. The accrual method can offer a clear picture of current and projected financial performance during a specific timeframe, such as during a given quarter. The biggest downside to the accrual method is that it can be relatively complex. Inherent to the accrual method are complicated functions such as accounts payable and receivable. Because of its complexity, the accrual method is recommended for larger companies with the ability to outsource their accounting to professionals.

The cash method is much simpler than the accrual method. Under the cash method, expenses and revenue are only recorded when the cash is on hand. While some industries, such as the agriculture industry, prefer the cash method, the healthcare industry lends better to the accrual method because payments can sometimes take months to be received.

In the healthcare industry, all accounting must follow the Generally Accepted Accounting Principles (GAAP) guidelines to avoid the aforementioned fees, fines, and criminal charges. GAAP refers to a common set of accounting principles, standards, and procedures issued by the Financial Accounting Standards Board (FASB). GAAP-compliance is usually determined by an external audit.

There are ten main principles of GAAP:

– The Principle of Regularity: the adherence to GAAP rules and regulations as a standard.

– The Principle of Consistency: the application of the same standards throughout the reporting process to ensure financial comparability between periods.

– The Principle of Sincerity: the provision of an accurate and impartial depiction of a company’s financial situation.

– The Principle of Permanence of Methods: the commitment to using procedures used that are consistent, allowing comparison of the company’s financial information.

– The Principle of Non-Compensation: the reporting of both positives and negatives with full transparency and without the expectation of debt compensation.

– The Principle of Prudence: the commitment to using fact-based financial data representation without speculation.

– The Principle of Continuity: the commitment to operating a business while simultaneously valuing assets.

– The Principle of Periodicity: the reporting of revenue during the appropriate accounting period.

– The Principle of Materiality: the commitment to fully disclose all financial data and accounting information in financial reports.

– The Principle of Uberrimae Fidei (utmost good faith): the commitment to honesty in all transactions.

All publicly-traded companies must adhere to GAAP, per the Securities and Exchange Commission (SEC). While not required by law for non-publicly traded companies, GAAP compliance is critical for favorable views from creditors and lenders. Most banks and financial institutions require GAAP-compliant financial statements when issuing business loans.

As is the case with other entities following GAAP, healthcare companies are required to produce financial reports and documentation indicating financial performance. These reports will include cash flows, balance sheets, and statements of operations and changes in net assets. Performance reporting provides important information for hospital trustees, senior management, and the general public.

Tax-exempt hospitals and healthcare services must also report their performance by itemizing uncompensated community care benefits.

In addition to generalized GAAP principles, hospitals and healthcare services must contend with several industry-specific concepts:

Many assets core to the healthcare industry are known as depreciating assets. These include commercial buildings, equipment, technology, software licenses, and IT infrastructure. When accounting for asset depreciation, you must report both the asset’s cost and useful life. Then, the asset’s depreciation expense will be recorded across each relevant accounting period.

Hospitals and healthcare services offer a wide variety of services to patients. Because of this, there are several different ways they can be reimbursed for the services in question:

– Capitation is a payment arrangement which entails an enrolled person paying a set amount per a specified period, such as a month or a year. The payments occur whether the enrolled person seeks care or not. The average expected health care usage of the enrolled person determines the payment amount.

– Per Diem is a payment that is based on the number of days a patient has received care. The per diem amount is typically set by the payer or determined through Medicare Severity Diagnosis Related Groups (MS-DRGs).

– Pay for Performance (P4P), also known as value-based purchasing, offers financial incentives to hospitals and healthcare services. Key performance indicators that determine P4P tend to be measurable, such as successfully lowering a patient’s blood pressure. P4P can place a significant burden on accounting as it is the least standardized payment model in the healthcare industry.

There are several challenges unique to receivables in the healthcare industry. When hospitals or healthcare services receive payments from insurers, the funds received are often only a portion of the services rendered and the outstanding amount is left as a receivable.

Additionally, payers often have unique pay schedules, which adds complexity to reporting revenue. Healthcare accountants must keep track of many different billings, receivables, and allowances.

Most hospitals and healthcare services are paid by both public and private entities; large hospitals or services may receive revenue from over a hundred different payers. Accounting for each type of payer is imperative to big and to small business profitability alike.

Transparency is a major facet of healthcare accounting, especially when it comes to payer mixes; people need to know what providers charge for payers. To determine prices, some hospitals will use a chargemaster — a comprehensive list of items billable to a patient or provider — or MS-DRGs to determine prices. Because of the many variables that go into healthcare costs, healthcare accounting can be an extraordinarily complex process.

Sometimes, the amount collected from payers and patients is greater than the amount owed. When this happens, credits accumulate in the accounts receivable. To alleviate the accumulation of credit, accountants can write outstanding checks. This is not uncommon.

In certain circumstances, the intended recipients of outstanding checks have passed away or are otherwise unable to receive the check. In this case, the accountants must turn over the uncollected funds to the state, per unclaimed property laws.

Due to the sheer number of moving parts, including federal and state regulations, to contend with, it isn’t difficult to see why errors can plague a hospital’s financial statements. Here are a few of the most common healthcare accounting mistakes — and how to avoid them.

In the past, most third-party payer contracts were written as a percentage arrangement. In recent times, however, payers have developed their own fee schedules. These fee schedules vary from payer to payer and can lead to a veritable accounting headache. Due to operating on an accrual basis where revenues and expenses are reported without having the cash in hand, it is entirely possible to misstate allowances in the revenue cycle.

A way to combat this is to implement a revenue cycle tool that can track billing, payments received, allowances, and other financial data. This will provide hard data, which leaves little room for error when determining how much will be received.

When it comes to accounting for healthcare, the game is always changing. Not keeping up-to-date on new accounting pronouncements can be an incredibly costly mistake for hospitals to make. For example, when it became no longer possible to classify bad debt expense and an operating expense, many hospitals failed to heed the pronouncement and faced financial consequences.

Accounting pronouncements usually come with some advanced notice. Financial teams should be proactive and keep their ears to the ground. They should also mark upcoming pronouncements on their calendars. For example, the AICPA tends to update their Audit and Accounting Guide each November at a conference. Accounting professionals should prepare to learn new guidelines each November.

Ignoring a problem won’t make it go away, especially in accounting. And when — not if — credit accumulates in the accounts receivable, ignoring or forgetting about it is the worst thing to do. Hospitals do not want to over or under-report revenue as this violates GAAP — and some larger hospitals can rack up credit balances well into the millions.

As previously mentioned, hospitals can alleviate accumulating credit balances in the accounts receivable by writing checks for outstanding amounts. These checks reimburse both patients and insurers. But even if a hospital is on top of their credit balance, checks must still be tracked. Recipients may move out of the country or pass away, leaving the hospital with a growing amount of outstanding checks, which reduces the balance on financial documents such as the balance sheet. Additionally, several states have unclaimed property laws that obligate the hospital to turn over old, outstanding checks to the state government.

To combat this, hospitals and healthcare services must be proactive in eliminating credit balances. Having someone on the financial team solely dedicated to solving credit balances is a must to avoid state or federal audits.

Physical expansion is a key indicator of hospital health. But if a hospital is building a new parking garage or wing, the financial team must be cognizant of debt obligations. For example, interest expense that a hospital pays on a debt obligation is not reflected as an interest expense on the income statement; it must be capitalized as a construction cost incurred during the construction period.

Due to the convoluted nature of healthcare accounting, having your accounts and books in order is imperative for the smooth running of any hospital or health service. However, it can also be tedious, complicated, and time-consuming. Additionally, the IRS can be unforgiving when it comes to mistakes — for example, filing your payroll taxes just one day past the deadline incurs a 2% penalty. These penalties can add up, too — up to a hefty 15% of the initial amount owed.

Outsourcing accounting and bookkeeping to an expert firm is a fairly simple and rewarding process that allows hospital and healthcare management to spend less time worrying over books and more time on day-to-day operations.

Every day, more and more small businesses make the switch to outsourced bookkeeping and accounting with FinancePal.

Jacob Dayan is a true Chicagoan, born and raised in the Windy City. After starting his career as a financial analyst in New York City, Jacob returned to Chicago and co-founded FinancePal in 2015. He graduated Magna Cum Laude from Mitchell Hamline School of Law, and is a licensed attorney in Illinois.

Jacob has crafted articles covering a variety of tax and finance topics, including resolution strategy, financial planning, and more. He has been featured in an array of publications, including Accounting Web, Yahoo, and Business2Community.

Nick Charveron is a licensed tax practitioner, Co-Founder & Partner of Community Tax, LLC. His Enrolled Agent designation is the highest tax credential offered by the U.S Department of Treasury, providing unrestricted practice rights before the IRS.

Read More

Jason Gabbard is a lawyer and the founder of JUSTLAW.

Andrew is an experienced CPA and has extensive executive leadership experience.

Contact us today to learn more about your free trial!

By entering your phone number and clicking the "Get Custom Quote" button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.

By entering your phone number and clicking the “Get Started” button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.