Let’s face it: unless you’re a certified accountant, filing taxes for any type of work can be a daunting task. The forms are confusingly named and perplexingly organized. Plus, amongst all those little oddly named boxes and complex legal jargon lies a lot of opportunity for mistakes. And the consequences for misfiling aren’t exactly laughable. It’s a source of stress for so many Americans in the workforce.

But for freelancers, the complexity of filing freelance taxes can increase tenfold. There’s no other party to provide most of your tax information for you; in many ways, you’re on your own.

If you’re facing tax filing for freelance work and are finding yourself fraught with fright, you’re in luck. This is your ultimate guide to filing your freelance taxes, so that you can rest assured that you’ll make it through tax season penalty-free.

Click on a link below to jump straight to the topic you’d like to learn more about.

In the eyes of the IRS, freelancers are business owners. That may sound weird to someone doing freelance writing on nights and weekends to make a little cash on the side, but it’s because freelancers are self-employed. That makes you an employer, even if the only employee is yourself.

Many Americans who are placed in a more traditional employer/employee situation don’t really understand taxes. They’re simply subtracted from paychecks on a regular basis and reported at the end of the year. But as a freelancer, it’s vital that you understand how taxes work to insure that you’re paying them correctly.

The basics of taxes are this: every working person, no matter their employment situation, pays income tax, which is a fixed percentage of their income. But that’s not the only type of tax that Americans are responsible for.

If you’re an employee, then your employer automatically takes 7.65% out of every paycheck to pay for both Social Security and Medicare taxes. These taxes come out gradually throughout the year with every single paycheck. The employer then pays an additional 7.65% towards the two on their own behalf, totaling 15.3% of your total income for Social Security and Medicare each year.

Here’s where things get expensive for freelancers come tax season. As a freelancer, you are considered both an employer and an employee. That means that, in addition to paying your income tax, you’re responsible for both the employee and the employer portions of Social Security and Medicare taxes, the entire 15.3% of your self-employed income.

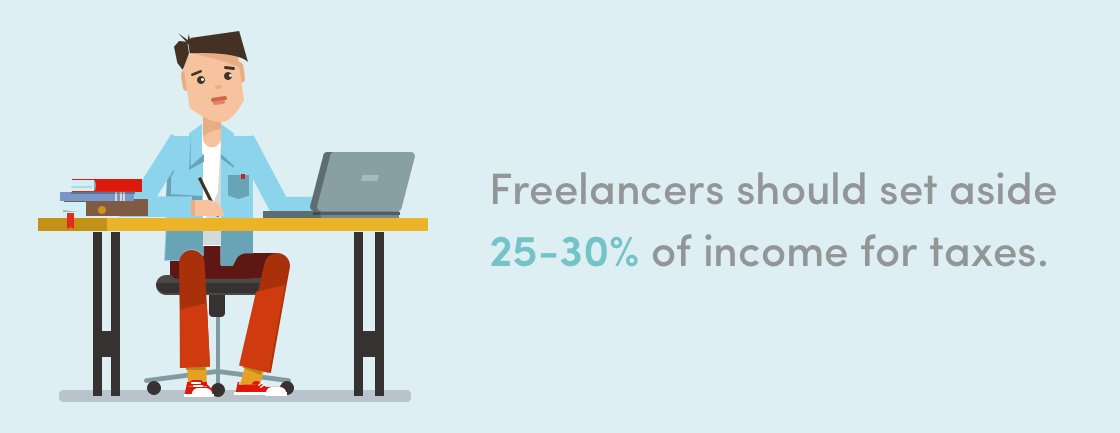

On top of that, you’ll be paying them in a lump sum, rather than having them removed little by little from your regular paycheck. Add all these percentages up, and you’re looking at a pretty big chunk of your freelance income. Most people estimate around 25% to 30% of your total freelance income will likely go towards taxes.

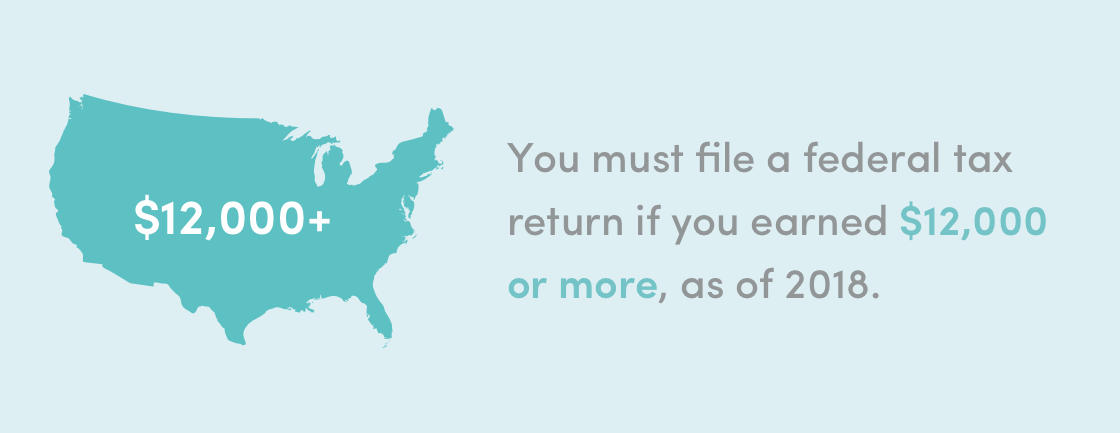

While the threshold for income taxes begins at $12,000 annual income, the threshold for freelancers to begin to pay taxes is much, much lower. Just how low, you ask?

A measly $400.

$400 is the minimum amount of income a person must make in order to be eligible for self-employment taxes (the Social Security and Medicare taxes mentioned above). Once you cross that income threshold through freelance work, self-employment taxes are instated. Note that this is only 15.3%; you still will not be required to pay income tax until you reach the $12,000 threshold.

Don’t forget that we’re talking about $400 gross income here. As a freelancer, you likely have at least some expenses related to your business (we’ll go into details on expenses later). Remove the cost of these expenses before determining whether you’ll need to file for taxes. If the amount of money you made minus the amount that went toward expenses is under $400, no need to file taxes.

As a standard employee, most of paying, preparing, and filing for taxes is done for you. Social Security and Medicare taxes are taken from each paycheck, your employer sends you any necessary documents each tax season, and it’s just up to you to either pass along to your tax preparer or enter the information into a tax preparation software.

When it comes to freelancing, however, all of these duties fall upon your shoulders. As a freelancer, you’ll have to take a much more proactive role when it comes to taxes. And, as with many aspects of life as a freelancer, taxes become a substantially more complex. Here’s what to expect:

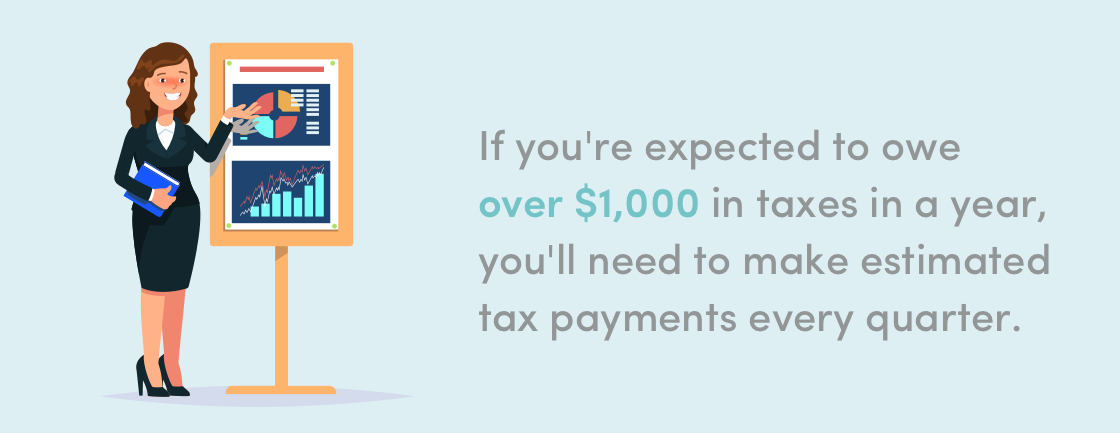

On a quarterly basis, you may need to begin making estimated tax payments to cover your self-employment tax. A general rule of thumb is that if you expect to owe over $1,000 come tax season, you’ll likely need to pay estimated taxes throughout the year. There are, of course, exceptions, so be sure to thoroughly read the eligibility requirements before making any payments.

It’s your responsibility to estimate the cost of your estimated tax payments, but you’re not totally on your own. IRS offers a specific worksheet, Form 1040-ES, for calculating estimated taxes. This form takes into account your expected adjusted gross income, taxable income, taxes, deductions, and credits throughout the year. The IRS suggests using your income, deductions, and credits for last year to help guide your estimations (though if this is your first year of freelance this may not help).

Unless your freelance income is even from month to month, it’s likely that you’ll need to re-calculate your estimated tax payments at least once throughout the year. If you find that your expected income earlier in the year was either too high or too low, simply complete Form 1040-ES again and adjust your estimated tax payments to compensate for the error.

Estimated tax payments only compensate for the self-employment taxes that your employer would be taking out of your paycheck on a regular basis. That means that, come tax season, you’ll still need to file for income tax.

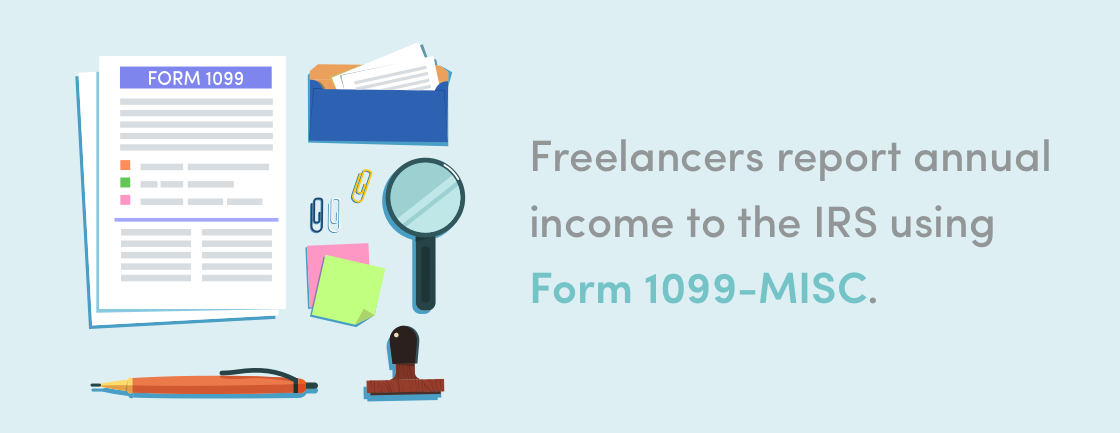

While you may be used to receiving a W-2 each tax season from your employer, as a freelancer, your income is reported on a Form 1099-MISC. Note that, even if your client doesn’t send you the form, you still need to file for that income. They’re only required to do so if they pay you more than $600—but you’re required to report on the income no matter the amount. That’s why it’s a good idea to always keep a record of your income from each client so that you’re not caught unprepared come tax season.

After calculating the above, we’re willing to bet you’re a little worried right now. For someone who is used to a W-2 tax filing, 30% of your income can feel like a pretty steep cost. But that’s where the fun part of freelance work comes in: deductions!

As a freelancer, and therefore a business owner, you have expenses related to your business that a standard employee doesn’t have. The funds you put toward these expenses are not considered income and can be deducted from the earnings you make via freelance work. As freelance taxes are based on your gross income (meaning your income minus the cost of your expenses), more expenses mean lower taxes.

The list of deductions you can claim for your business is extensive. Most things that enable you to run your freelance business can be claimed as deductions come tax season. This includes (but is not limited to):

Your Office

Your Office

Whether you rent an office or conduct your freelance business from your home, your office space can be claimed as a deduction on your taxes as long as it meets the following requirements:

1. You regularly use that room exclusively to conduct your business

2. That room is the principal place of your business

There are a few different ways to calculate your office deduction. The first way allows you to deduct a percentage of your mortgage/rent, property taxes, cost of maintenance, etc. based on the percentage of your home that is used for your business. If your home office is 5% of your total square footage, you can deduct 5% of the listed expenses.

If the above process sounds too complex, the IRS offers a simplified option for calculating your home office deduction. Simply deduct $5 per square foot of the space used for your freelance work (up to 300 square feet).

Your Car

Your Car

The use of your car for freelance-related work is a simple deduction for any freelancer. Most uses of your car that are related to your freelance business can be counted towards your deduction—whether that’s traveling to and from clients, purchasing products from vendors, or a number of other usages.

Calculating this deduction is pretty simple. You can claim around $0.54 for every mile you drive for your business. Simply keep track of the number of miles you drive, tally them, and multiply by the standard mileage rate to calculate your deduction.

Your Health Insurance Premiums

Your Health Insurance Premiums

As long as you’re not eligible for health insurance through your spouse’s employer, you’re likely eligible for deductions based on your health insurance premiums for you, your spouse, your dependents, and your children.

If you pay premiums out of your own pocket and they exceed 7.5% of your total income, you may be able to deduct the amount over 7.5% as a medical expense.

Your Continuing Education

Your Continuing Education

As a self-employed freelancer, you may (wisely) opt to continue your education. As long as your education “maintains or improves skills needed in your present work,” you may be able to claim these costs as a deduction. This can include:

The list of deductions that you can take for your business is extensive, each category with their own nuances for qualification. The best way to ensure that you’re taking advantage of all the deductions you qualify for—and none of the deductions you don’t—is by taking advantage of tax consulting services. Work with a professional to ensure that you’re filing correctly, and you’ll avoid the possibility of penalties down the line.

As with all tax documents, the 1099-MISC Form simply requires you to enter the requested information. The tricky part is knowing what to enter and making sure it’s correct. Let’s walk through the information requested in each box and how to complete it.

Here, you’ll enter the amount paid on any rent, as long as it’s $600 or more. This may include real estate rentals for office space, rentals of any sort of machinery, or land sure as pastures for grazing. Note that, if you paid rent to a real estate agent or property manager, you won’t need to report that on this form, as they’ll be reporting this payment themselves.

This box is for gross royalty payments of $10 or more. These may come from gas, oils, minerals, or other similar payments. Royalties can also be reported on intangible property (copyrights, patents, etc.) or publisher royalties for published works.

The “Other” box is exactly what it sounds like. Enter any income that isn’t requested and reported on in any other box of the form (as long as it exceeds the $600 minimum). This pay includes things such as:

Enter backup withholding and income tax withheld from payments to members of Native American tribes.

In the event that you work in the fishing industry, enter your share of proceeds from the sale of a catch or from distribution in kind. Also, report payments under $100 that were received for additional duties completed (though do not report any wages reportable on a W-2).

As a self-employed person, you’ll likely be making many more payments to medical and healthcare professionals than a more traditionally employed person. This box is used to report any payment of $600 or more to any provider of medical services, as well as insurance payments.

Here, you’ll enter any nonemployee compensation of, you guessed it, $600 or more! This is any compensation (fees, commission, prizes, awards, etc.) that you paid to an individual who completed services for you as a nonemployee. Typically, a payment qualifies as a nonemployee compensation when the following conditions are met:

This may include services such as the following:

As a general rule of thumb, if a payment can be reported elsewhere in your tax form 1099-MISC, it should not be reported on in Box 7. Do not report the following payments in Box 7:

Any total payment of at least $10 that was paid to a customer (an individual, trust, estate, partnership, association, company, or corporation) in lieu of dividends or interest as a result of a loan can be entered here.

If you sold consumer goods to another person for $5,000 or more outside of a retail establishment, enter an X in this box. If this sale was made in a store or any other permanent retail establishment, do not check this box.

For any payments that are made to farmers by insurance companies of $600 or more.

A golden parachute payment is any payment that meets the following conditions:

An excess golden parachute payment is the amount of the payment that exceeds the individual’s salary. So, if the individual’s salary was $200k and the payment was for $1m, the excess golden parachute payment would be $800k.

Again, these must be for $600 or more to qualify.

Does filing freelance taxes sound complex? That’s because, truthfully, it is! Freelancers have so much to worry about as is, from completing work and managing invoicing and payments to balancing numerous projects, personalities, deadlines, and more. Managing your own freelance taxes is a complex piece of the puzzle that, frankly, you could probably do without.

Even more intimidating are the consequences of filing wrong. Regardless of whether your mistake is accidental or intentional, the IRS will still hold you to penalties in the event that something is incorrect.

Our advice? Don’t go at it alone. There are tax preparation services at your fingertips, full of tax professionals who have dedicated their lives to helping freelancers and small businesses like you manage their taxes. We’ll take care of tax preparation for small businesses, to take a bit of the stress off your shoulders. Contact us today for help.

Jacob Dayan is a true Chicagoan, born and raised in the Windy City. After starting his career as a financial analyst in New York City, Jacob returned to Chicago and co-founded FinancePal in 2015. He graduated Magna Cum Laude from Mitchell Hamline School of Law, and is a licensed attorney in Illinois.

Jacob has crafted articles covering a variety of tax and finance topics, including resolution strategy, financial planning, and more. He has been featured in an array of publications, including Accounting Web, Yahoo, and Business2Community.

Nick Charveron is a licensed tax practitioner, Co-Founder & Partner of Community Tax, LLC. His Enrolled Agent designation is the highest tax credential offered by the U.S Department of Treasury, providing unrestricted practice rights before the IRS.

Read More

Jason Gabbard is a lawyer and the founder of JUSTLAW.

Andrew is an experienced CPA and has extensive executive leadership experience.

Contact us today to learn more about your free trial!

By entering your phone number and clicking the "Get Custom Quote" button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.

By entering your phone number and clicking the “Get Started” button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.