At FinancePal, we recognize that most small business owners started their companies because they were experts in providing a good or a service—not at balancing a book. Plus, accounting and bookkeeping for startups can be complex and multi-faceted. That said, sound accounting and bookkeeping are imperative to manage any company’s financial health, guide decisions for growth initiatives, and ultimately ensure your business is in good standing with its tax obligations throughout the year.

Industry jargon and complex language provides a significant obstacle for most people when trying to learn accounting concepts. That is why we provided this glossary of accounting industry terms from ecpi.edu to gain a solid baseline from which you can explore various accounting topics.

Money a business owes to its suppliers, vendors, or creditors for goods or services bought on credit; considered a short-term debt. Accounts payable is a crucial concept for any business operating with credit—every time a business purchases from a supplier on credit, an accounting entry is made in accounts payable.

The opposite of accounts payable; money owed to a business by its customers, for goods or services delivered. Accounts receivable refers to money your customers owe for goods or services purchased from you in the past. This money is typically recorded as an asset on your balance sheet; they live under the ‘current assets’ portion on your balance sheet or chart of accounts.

An accounting period is a period during the fiscal or calendar year in which accountants perform functions such as gathering and aggregating data and creating financial statements. The financial statements made during these periods are important for attracting potential investors or procuring loans from banks.

A record-keeping adjustment that recognizes business expenses and revenues before exchanges of money take place.

An accounting method where revenue and expenses are recorded as they are earned, regardless of when the money is received or paid. Mutually exclusive with cash-basis accounting.

Resources with economic value. Assets can reduce expenses, generate cash flow, or improve sales for businesses.

A financial statement providing a picture of an organizations’ liabilities, assets, and shareholders’ equity at a specific moment in time. Compare the balance sheet vs. income statement.

A person’s or organization’s financial assets. Capital may include funds in deposit accounts or money from financing sources.

Under the cash method, income is considered constructively received the moment it is credited to a business’s account, made available without restriction, or received by an authorized agent acting on behalf of the company.

Cash flow is the total amount of money that comes into and goes out of a business.

Certified public accountants (CPAs) are accounting professionals certified to practice public accounting by the American Institute of Certified Public Accountants.

An index of the financial accounts in a company’s general ledger, a chart of accounts provides a picture of all the financial transactions a company has conducted in a specific accounting period.

An idiom refers to accounting for all financial transactions within a certain period.

Cost of goods sold, commonly shortened to COGS (or, if applicable, referred to as cost of sales or cost of service), is simply how much it costs to produce products or services, including direct material or labor expenses. Cost of goods only includes expenses directly related to products and services. For example, a chandler business would consist of wax, wicks, glass, and ingredients in its COGS. Overhead, such as marketing spend, real estate, utilities, asset depreciation, shipping fees, and other indirect expenses do not count towards COGS.

Credits are accounting entries that either increase an equity or liability account, or decrease an expense or asset account.

The opposite of a credit, debits either increase expense or asset accounts or decrease equity or liability accounts.

The depreciation accounting method determines the decreasing value of a tangible asset over its lifetime.

Diversification mixes many different investments and assets in one portfolio, allowing individuals or businesses to spread out risk and protect themselves from financial ruin if any investments or assets fail. Finance Pal’s own CEO and Co-founder, Jacob Dayan, provides his expert investment advice on Finder’s “11 pieces of investment advice from experts for beginners” to provide individuals guidance to the best investment plan.

Company earnings, or profit, which a business pays to its shareholders as a reward for their investment in its equity.

Put simply; double-entry accounting is a ubiquitous bookkeeping system that tracks where the money comes from and where it goes. The central tenet of double-entry accounting is after a financial transaction, each entry made into an account has a corresponding opposite entry made into a separate account. This produces two entries—thus, the name. When shown side-by-side in a ledger, the entry listed on the left side is referred to as a debit entry, while the entry displayed on the right side is called a credit entry.

Federally licensed tax professionals who can represent U.S. taxpayers. They must pass the three-part special enrollment examination from the IRS.

Entity formation is the process of classifying a business as an entity such as an LLC, sole proprietorship, partnership, S-Corp, or C-Corp.

The costs of conducting business. Companies can deduct some eligible expenses from their taxes.

The amount of money left over and returned to shareholders after a business sells all assets and pays off all debt.

A type of expense, fixed costs do not change from month to month. Fixed costs include things like payroll, rent, and insurance payments.

General ledgers include debit and credit account records. Companies use the information in their general ledgers to prepare financial reports and understand their financial performance and health over time.

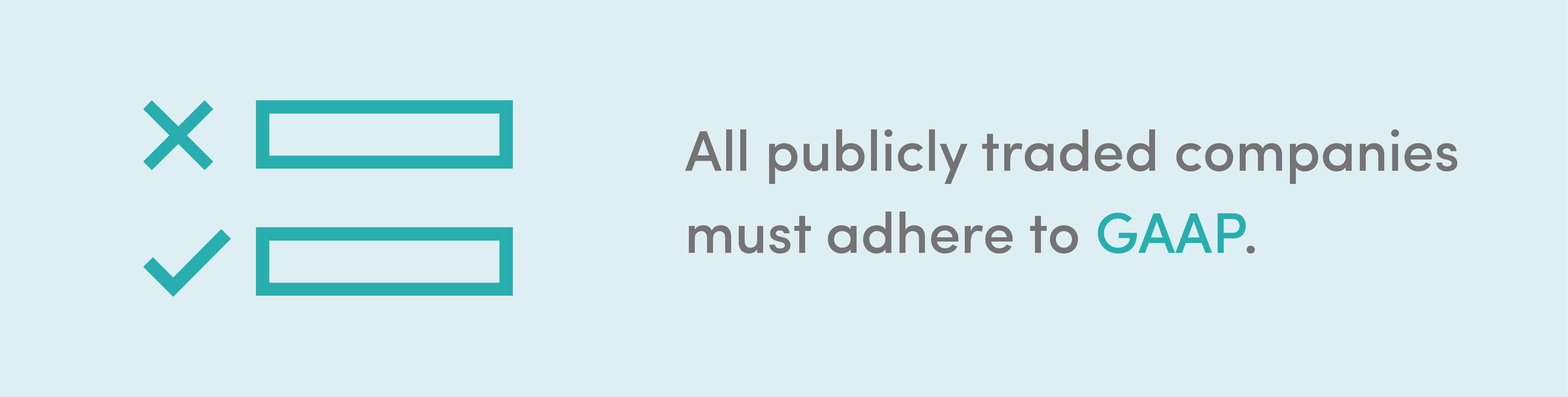

Generally accepted accounting principles (GAAP) refer to a group of significant accounting rules, standards, and ways of reporting financial information. The Financial Accounting Standards Board sets GAAP. All publicly traded companies must adhere to GAAP, per the Securities and Exchange Commission (SEC). While not required by law for non-publicly traded companies, GAAP compliance is critical for favorable views from creditors and lenders. Most banks and financial institutions require GAAP-compliant financial statements when issuing business loans.

The profit businesses make after subtracting the costs related to supplying their services or making and selling their products.

A business’s net sales revenue after subtracting the costs of goods sold. It represents the revenue companies keep as gross profit. An indicator of financial health, higher gross margins typically mean that a company can make more profit on its sales. Lower gross margins may mean a business needs to reduce production costs. The formula for gross margin is “Gross Margin = Net Sales – Cost of Goods Sold.”

A company’s goods and raw materials used for making the products it sells. It appears on a balance sheet as an asset. The IRS permits several inventory cost methods depending on the type of inventory (for example, FIFO or LIFO). A small business accountant will know which method the IRS requires for each specific business. Using the appropriate method, the accountant will calculate your inventory cost and set the cost of goods sold formula into motion.

A business transaction recorded in a business’s general ledger.

A liability is when someone owes someone else money. Types of liabilities can include loans, mortgages, accounts payable, and accrued expenses.

How easily an individual or business can convert an asset to cash for its full market value. The most liquid asset, cash, can easily and quickly convert to other assets.

The amount an individual or business earns after subtracting deductions and taxes from gross income. To calculate the net income of a business, subtract all expenses and costs from revenue.

An agreement for an individual or company to pay for a good or service later. Usually an invoice will be sent with payment due at a later date.

The ongoing costs of doing business other than those related to directly creating a good or service.

HR and accounting departments typically handle payroll, the total compensation a company pays its employees for a specific time period.

The notion that money is worth more today than it will be in the future. This may seem confusing at first, so let’s look at an example: if you have ten thousand today, you can invest the money, earn interest, and have more than ten thousand dollars in five years. The discounted cash flow model accounts for this, so it can also help compare different investment opportunities.

The profit and loss statement (also called the income statement or shortened to “the P&L statement”) includes vital cash flow information such as revenue, costs of goods sold, and operating expenses during a particular period. It also shows the resulting net income or loss for that specific period.

Written notices acknowledging that one party received something of value from another. An acknowledgment of ownership, receipts are proof of a financial transaction.

The amount of net income left for a business to use after paying dividends to its shareholders. A company’s management typically decides whether to keep the earnings or give them to shareholders.

The efficiency of an investment, including the amount of return on an investment relative to its cost. Accountants can also use ROI to compare the efficiency of more than one investment. To calculate ROI, subtract the cost of investment from the current value of investment, and divide that by the cost of the investment.

Gross income a business makes through normal business operations. To calculate sales revenue, multiply sales price by number of units sold.

Small business sales tax is an indirect tax that is assessed on a product at the point of sale. Included within the price of the product.

A type of accounting system that records the financial transactions of a business. The system uses one entry per transaction to record cash, taxable income, and tax-deductible expenses going in or out of the business. Businesses can use accounting software or even simple tables to perform single-entry bookkeeping.

A periodical bookkeeping worksheet, a trial balance compiles the balance of ledgers into credit and debit columns that equal each other. Companies create trial balances to ensure the mathematical accuracy of their bookkeeping systems entries.

Expenses that change depending on the level of a business’s production. Variable costs go up when production increases and down when production decreases. In contrast to variable cost, fixed cost refers to expenses for a company that stays the same, regardless of production. Fixed costs may include insurance, rent, and interest payments.

Jacob Dayan is a true Chicagoan, born and raised in the Windy City. After starting his career as a financial analyst in New York City, Jacob returned to Chicago and co-founded FinancePal in 2015. He graduated Magna Cum Laude from Mitchell Hamline School of Law, and is a licensed attorney in Illinois.

Jacob has crafted articles covering a variety of tax and finance topics, including resolution strategy, financial planning, and more. He has been featured in an array of publications, including Accounting Web, Yahoo, and Business2Community.

Nick Charveron is a licensed tax practitioner, Co-Founder & Partner of Community Tax, LLC. His Enrolled Agent designation is the highest tax credential offered by the U.S Department of Treasury, providing unrestricted practice rights before the IRS.

Read More

Jason Gabbard is a lawyer and the founder of JUSTLAW.

Andrew is an experienced CPA and has extensive executive leadership experience.

Contact us today to learn more about your free trial!

By entering your phone number and clicking the "Get Custom Quote" button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.

By entering your phone number and clicking the “Get Started” button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.