It is common to feel guilty for procrastinating, but the vast majority of people do it. According to a study conducted by entrepreneur and author Darius Foroux, 88% of the 2,219 respondents admitted to procrastinating. And when it comes to taxes, people are no different. However, with taxes, there is a hard deadline that you cannot miss. So how late is too late to file? This article breaks it down.

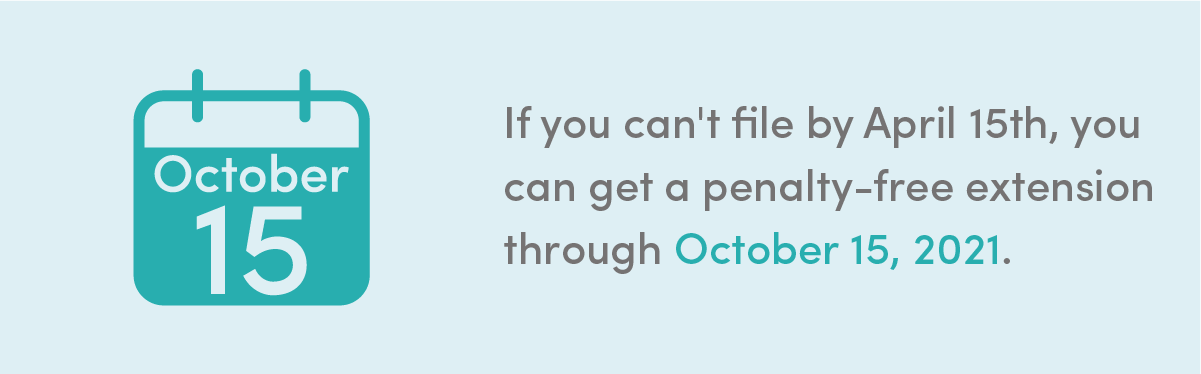

A common saying goes, “The best time to file your taxes was the week filing opened. The second best time is right now.” But if you insist on procrastinating, the federal tax deadline for the 2020 tax year is April 15, 2021. In most circumstances, any taxes filed after the deadline are filed too late and open up the possibility for penalties, fines, or substitute returns. However, if you file for an extension, the deadline is pushed back to October 15, 2021. We will go over filing for an extension in more detail later.

The consequences vary depending on whether you owe the IRS taxes or the IRS owes you a refund.

Either way, the IRS will file a Substitute for Return (SFR) on your behalf. A Substitute for Return is based solely upon information the IRS already has and is often not optimized for the best return; you will not be eligible for any exemptions, credits, or favorable deductions. If the IRS owes you a refund, you can still file a return to replace the SFR to obtain this refund — and it is better to do this sooner rather than later to avoid additional penalties.

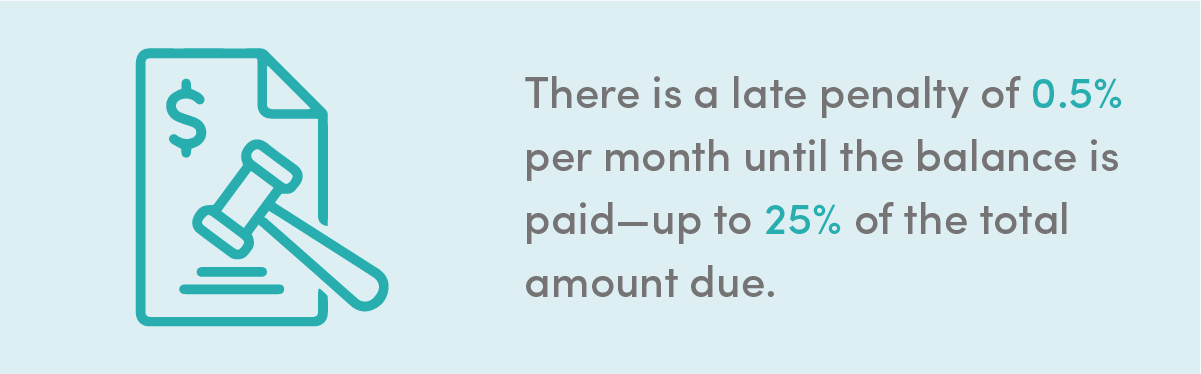

If you owe a balance to the IRS based on the SFR, things can get a little dicey. There is a late penalty of 0.5% per month until the balance is paid — up to 25% of the total amount due. You will also owe interest on the outstanding balance at the time of the deadline.

As previously mentioned, filing for an extension will push the deadline back to October 15, 2021. If filed before the tax deadline, you will not have to pay penalties or fees unless you miss the October 15 deadline.

While it is always best to file your returns by the original deadline, extenuating circumstances may make this problematic. If you cannot physically meet the original deadline, please file an extension before April 15, 2021.

You can read more tax information here.

Nobody falls behind on their taxes on purpose; owing the IRS is often the result of several unfortunate circumstances coming to a head simultaneously. The most common reasons for owing back taxes are changes that make it challenging to pay off your original balance, such as divorce, reduction in income, or job loss. And once the notice comes in the mail, it can seem like just another blow in a losing fight.

Our perceptions of the IRS are mostly shaped by word of mouth. Many Americans perceive the IRS as an inexorable, monolithic organization bent on getting their due one way or another. In truth, they are a fair creditor and want nothing more than delinquent taxpayers to return to good standing. To facilitate this, they have instituted several programs over the years aimed at getting down-on-their-luck taxpayers back on their feet. Chief among these programs is the Fresh Start Initiative.

The IRS has several restrictions for who is and isn’t eligible for the Fresh Start Program:

Having your books in order is imperative for any small business owner. However, it can also be tedious, complicated, and time-consuming. Additionally, the IRS can be unforgiving when it comes to mistakes — filing your payroll taxes just one day past the deadline incurs a 2% penalty. These penalties can add up, too — up to a hefty 15% of the initial amount owed.

Outsourcing accounting and bookkeeping to an outside firm is a relatively simple and rewarding process that allows business owners to spend less time worrying over books and more time running the business. Expert accountants can take care of tax preparation, payroll, tax consulting, and more. Every day, more and more small businesses make the switch to outsourced bookkeeping and accounting with FinancePal.

Jacob Dayan is a true Chicagoan, born and raised in the Windy City. After starting his career as a financial analyst in New York City, Jacob returned to Chicago and co-founded FinancePal in 2015. He graduated Magna Cum Laude from Mitchell Hamline School of Law, and is a licensed attorney in Illinois.

Jacob has crafted articles covering a variety of tax and finance topics, including resolution strategy, financial planning, and more. He has been featured in an array of publications, including Accounting Web, Yahoo, and Business2Community.

Nick Charveron is a licensed tax practitioner, Co-Founder & Partner of Community Tax, LLC. His Enrolled Agent designation is the highest tax credential offered by the U.S Department of Treasury, providing unrestricted practice rights before the IRS.

Read More

Jason Gabbard is a lawyer and the founder of JUSTLAW.

Andrew is an experienced CPA and has extensive executive leadership experience.

Contact us today to learn more about your free trial!

By entering your phone number and clicking the "Get Custom Quote" button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.

By entering your phone number and clicking the “Get Started” button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.