Real estate is one of the most lucrative markets in the world. It’s also one of the most complicated. There’s an enormous amount of speculation in the housing market. Not only that, but it’s generally agreed upon that if you want to turn a profit and generate substantial wealth, you must invest in a multitude of properties. That’s a lot of assets, a lot of speculation, and a lot of numbers to crunch; and that’s why having accurate accounting is a must.

It’s easy to think of accounting as a backroom chore, a tedious task that only serves to protect you from the IRS. In actuality, good accounting is your ticket to better financial decision-making, increased cash flow, and improved asset management.

Regardless of your position in the real estate field, let this guide on real estate accounting be your ultimate asset in your effort to maximize your assets. The first few sections will detail general accounting practices across all industries, just in case you need to freshen up on Accounting 101. Afterward, we’ll detail the ins and outs of accounting for real estate professionals—practices that are more unique to the real estate field.

The federal government mandates that private companies follow specified standard accounting practices. The purpose of these accounting regulations is to:

Accounting standards are set by the nonprofit organization, Financial Accounting Standards Board (FASB). The Securities and Exchange Commission (SEC) designated FASB the official standard-setter of United States accounting practices, so FASB standards are generally seen as authoritative. You can review these standards on the FASB website.

Can you get in trouble for erroneous or misleading accounting practices? Yes. Honest mistakes do happen, and honest mistakes may be amended. But intentionally manipulating financial information is considered a white collar crime and may warrant prosecution. Don’t say you weren’t warned.

American accounting has an enormous amount of rules and requirements. They’re important regulations, but they can also be overwhelming, especially if your real estate business is small. If you’re not sure where to get started, here’s some friendly advice—hire an accounting service for real estate professionals.

You might be reading this guide because you’re intent on doing the accounting yourself. We commend the bravado. Remember, though, that keeping records of real estate transactions is a massive and never-ending task, and you could seriously damage your company’s financial standing with any errors. Accountants are trained in the business of bookkeeping (they often spend years in school studying the ins and outs), and they have sufficient know-how to perform accounting work faster and more accurately than you can.

Still not convinced? That’s all right. We’ll try and convince you several more times throughout this guide.

Parties who may wish to view accounting records include:

While financial reports are made to the IRS during tax season, the IRS may request more detailed financial records if your company is selected for audit.

Bookkeeping is the recording of all your company’s financial transactions (accountants rejoice, bookworms sigh). Accurate bookkeeping is the foundation of good real estate accounting (and it’s something you’ll want to uphold, unless you enjoy IRS audits).

Get to know the double-entry bookkeeping system. This is a system of accounting in which each transaction results in two entries being made: a debit and a credit. These have nothing to do with debit cards or credit cards; we’ll refer to “debit” and “credit” by their accounting context:

Imagine that you have an open book in front of you—a business ledger. Let’s say that you collect $500 rent from a tenant. In traditional bookkeeping, you would enter the debited amount on the left page, and the credited amount on the right page. So, for this transaction, $500 would be recorded on the left page (debit) and $0 recorded on the right page (credit).

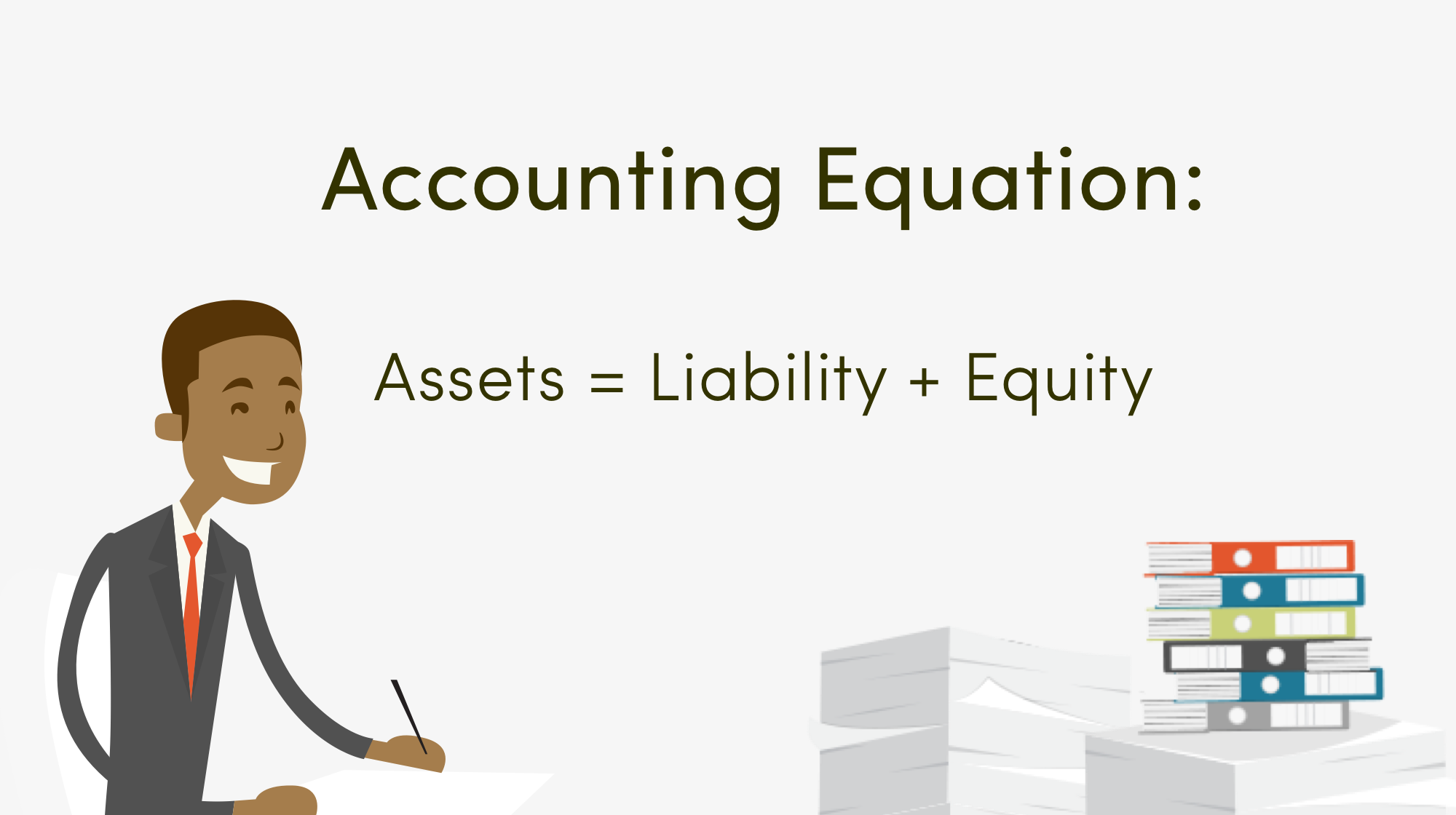

What’s the benefit of this system? For one, it makes for a very helpful equation (known as the accounting equation):

Assets = Liability + Equity

The combined liability and equity amounts must equal the assets. If the numbers don’t match, then there has been an accounting error. Granted, there could still be an error even if the equation is balanced (for instance, if two separate errors offset one another). But the accounting equation is a good way to detect glaring errors.

We’ll cover “assets”, “liability”, and “equity” in the next section.

Nowadays, the term “bookkeeping” refers only to the accounting practice—you don’t actually have to keep transaction records in printed business ledgers. Nonetheless, that’s still how many modern businesses choose to do it. Books, books, books, and filing cabinets; it’s worked for centuries, and it still does today.

Digital bookkeeping, however, has taken the accounting world by storm. Modern software exists that digitally records each transaction and performs calculations.

What’s nice about digital accounting is that it’s much easier to find transaction information than in traditional bookkeeping. Let’s say that you wanted to review transactions made on March 9, 2016. If you’ve been bookkeeping by the books, you’d have to sift through your cluttered filing cabinet, find the “March 2016” ledger, and flip, flip, flip through the pages to find March 9 (it’s even more tedious if you have multiple ledgers for March 2016). But, when the records are stored digitally, all you’ve got to do is enter a few words into the search bar.

If you’re running a small real estate business, you might have to wear many different hats due to lack of manpower. If you’re wearing many hats, it’s easy to fall behind on your bookkeeping—especially given how many small costs and fees that are part of a single real estate transaction.

Again, an accountant can do wonders for you. The right accountants should have no problem assisting you with catch-up bookkeeping, especially if it’s a finance company that has multiple accountants it can place on your books.

Within accounting, there are 5 elements that are affected by transactions:

By accounting for all 5 of these elements, you’ll have a complete grasp over your company’s finances.

An asset refers to something the company owns and uses for the benefit of the company. So long as it can generate cash, it can be considered an asset. There are 2 types of assets:

In real estate, properties are the principal assets.

When accounting for assets, it’s important to have recorded “accounts receivable”. This term simply refers to money that is owed to the company.

A liability is basically the opposite of an asset. Liability refers to the money that the company owes. Just like an asset, there are 2 principal types of liabilities:

When accounting for liabilities, you’ll have to record “accounts payable”. This term refers to all the outstanding debt that the company owes.

In real estate, mortgages are a common liability.

Equity determines the value of the company when accounting for the difference between assets and liabilities. Here’s the equation:

If the company has multiple owners, each may have a different amount of equity in the company—which must be accounted for separately.

Any time you charge for a good or service, the cash you recieve is income. In real estate, you might gain income by collecting rent from a tenant.

If you’re paying money—aside from debt—then you’re paying an expense. For example, if you own a real estate brokerage, the income of your staff would be accounted as an expense (if your staff is on salary, the expense might also be accounted as a liability).

Good accounting should ultimately help you save money on taxes. If you’re going to maximize your tax savings, you should know a few of the taxes that are relevant to real estate.

The value of a property measures the overall worth of a property. A real estate valuation is not a property tax, but it does have a substantial effect on your taxes. The four elements of value are:

The appraisal is done by an assessor. The assessor may use a few different methods to determine the value of a property, including:

Familiarize yourself with these methods if you want to manipulate your property so that it may be valued higher or lower. Remember, too, that value also measures the property’s future worth; be aware of impending:

The real estate tax is widely referred to as the “property tax”. This is a tax on immovable property—like a house, commercial building, or plot of land. The real estate tax is based heavily on your property’s value. Other factors include:

Your property tax may vary from year to year, depending on changes among the above conditions and whether or not your property’s value is reassessed.

A personal property tax is a tax placed on “moveable” items on your property. If these items produce income for your company, they may be subject to a personal property tax. Your real estate business might have to pay taxes on tools, equipment, and vehicles that it owns, or perhaps even on any furniture you’ve placed in rental homes.

With proper foresight and planning, your real estate business could capitalize on numerous tax benefits. That’s why having strong accounting is important. There are a few important areas to consider when planning for tax savings.

Assets—like a building—wear down over time, which may cause a natural loss in value. This is called depreciation. When you’re filing taxes, you can note depreciation of a property to protect your income. The depreciation amount is determined through a calculation. You can subtract the depreciation amount from your total taxable income, and that can save you a good deal of money.

If your business owns rental properties, you could benefit from a large number of tax savings, like:

Capital gains is a tax that’s levied on the profit you make from the sale of an asset. The capital gains tax may be higher or lower depending on how long the asset was owned prior to the sale. The best way to avoid or reduce capital gains taxes is to be strategic about when you sell an asset. An experienced, tax-saving accountant can help you with that. We’ll go more into asset management in the next section.

Your business might be selected for audit by the IRS. The audit may be due to errors on your company’s tax filing, or perhaps the audit was selected at random. Either way, meticulous accounting may save you from heavy penalties or further inquiries. This is another area where you’ll benefit from having an accountant. Accountants may be trained in audit defense, and they’ll know how to properly handle dealings with the IRS, and get gathered any financial materials that are requested of you.

The most successful real estate businesses are able to maximize each asset’s profitability. This is where quality real estate accounting is a necessity. Your accounting should be concerned with:

If you own rental properties or if you’re in the property management business, your accounting should be concerned with tracking:

Many modern real estate businesses generate income through rental properties. Accurate accounting should help you determine whether or not a rental property is generating sufficient revenue; if it’s not turning a profit, perhaps it’s time to raise rent, raise the property value, redevelop the property, or sell the property.

On that note, accurate accounting may also help you make the best decisions when buying or selling assets. The books will shed light on a few important questions:

As you can see, accounting doesn’t only keep track of past financial records. It also helps you make the best decisions for your company’s future.

If you own a larger real estate company, you likely have staff that need to be compensated. Your staff may be comprised of hourly employees and salaried employees. But, in real estate, it’s very likely that some of your staff will work by commission. Accounting should track:

You also have to pay payroll taxes each year, so be sure to include that cost in your tax preparation.

Accounting covers a broad range of facets and tracks an overwhelming amount of financial numbers (which you’re no doubt aware of, since you’ve reached the end of this guide). If you run a small business or if you enjoy challenging yourself to such laborious tasks, you might be tempted to do all of your accounting on your own.

Again—and for the last time, we promise—we recommend enlisting the services of an accounting company. Accounting is a massive and massively important business endeavour. It’s all too easy to get behind on the books or to record inaccurate information—and don’t forget that your business may face severe financial penalties if you do.

If your business is involved in the real estate trade in any way, you could benefit tremendously from having an accountant that’s knowledgeable about the housing market. Some of those trades include:

For any business involved in these trades, an accountant can help to:

If possible, hire an accounting service that facilitates all the different aspects of accounting: tax preparation, audit defense, asset management, and staff accounting. These companies, like FinancePal, will shoulder nearly all of the accounting workload for you. That way, you can spend less time hitting the books, and more time finding, managing, and selling properties.

Jacob Dayan is a true Chicagoan, born and raised in the Windy City. After starting his career as a financial analyst in New York City, Jacob returned to Chicago and co-founded FinancePal in 2015. He graduated Magna Cum Laude from Mitchell Hamline School of Law, and is a licensed attorney in Illinois.

Jacob has crafted articles covering a variety of tax and finance topics, including resolution strategy, financial planning, and more. He has been featured in an array of publications, including Accounting Web, Yahoo, and Business2Community.

Nick Charveron is a licensed tax practitioner, Co-Founder & Partner of Community Tax, LLC. His Enrolled Agent designation is the highest tax credential offered by the U.S Department of Treasury, providing unrestricted practice rights before the IRS.

Read More

Jason Gabbard is a lawyer and the founder of JUSTLAW.

Andrew is an experienced CPA and has extensive executive leadership experience.

Contact us today to learn more about your free trial!

By entering your phone number and clicking the "Get Custom Quote" button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.

By entering your phone number and clicking the “Get Started” button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.