When you own a construction business, you have to deal with a lot of moving parts, from managing contracts and scheduling projects to basic business ownership responsibilities like hiring and filing taxes. Among this long list of responsibilities is accounting.

To help you structure your accounting in a way that keeps the best financial tabs on your business and maintains your compliance with financial recording requirements, we’ve created this guide on accounting for construction. In this post, we will cover the special considerations contractors need to take into accounting, as well as which accounting method you should use. For example, contractors should use cash-basis accounting instead of the accrual method because it allows you to record revenue when payment is received, establishing a clearer view of current cash flow.

For more tips like this, we recommend reading the post from start to finish for a full overview of the basics of accounting for contractors. If you already have a general understanding of accounting or are interested in a specific aspect of accounting for contractors, use the links below to navigate to the section that best answers your question.

For contractors (as well as all other business owners), accurate financial tracking and reporting is essential to the success of your business. Whether you are new to owning a construction business or are finding flaws in your current accounting system, understanding the basics of accounting for construction can help you structure your finances in a way that helps you minimize your business’s financial challenges.

Proper accounting for construction also helps to ensure that you are pricing your services fairly (for both you and your clients), maintain the profitability of your business, and can accurately plan for the future.

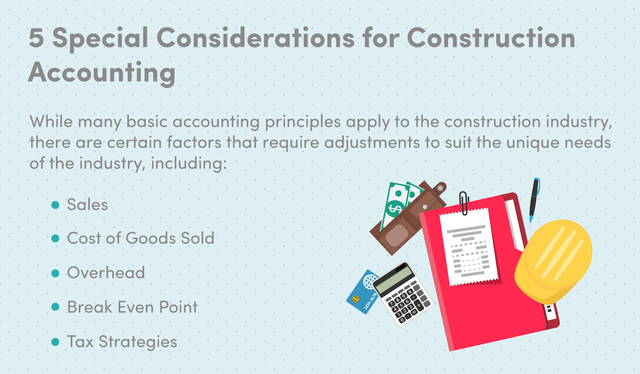

When setting up accounting for your contractor accounting system, there are certain factors you will need to pay special attention to based on the unique needs of your construction business:

Together, all of these factors will amount to better construction accounting that can strengthen your business’s financial health, both in the short-term and long-term.

Even the smallest mistakes in your bookkeeping and accounting could have long-lasting effects on the financial health of your business. For example, tracking costs incorrectly can lead to inaccurate estimates that cause you to lose money on projects.

Did you know that your accounting is more than just records you use to track costs and profits internally? From recording transactions as they happen and creating your financial statements for the period to filing your taxes, accurate accounting is critical. Complying with financial requirements is mandatory, and failing to do so could mean hefty fines or even seizure of your business.

As such, it is critical that you take the time to understand the nuances and best practices for accounting for construction.

However, before you can implement accounting processes, you first need to understand the differences between general accounting vs. construction accounting.

Let’s dive in…

It might seem like accounting is generally applied to all businesses the same way. However, each industry has distinct needs, including construction contractors. While many industries can apply general accounting to their business model, there are several adjustments necessary when it comes to accounting for construction. This is because there are little to no fixed costs—think mobile environments (working at job sites), unique projects, and the variations between types of contracts for different services and timelines.

One of the primary differences between construction accounting and general accounting is that contractor businesses are structured around projects. Because of this, there is a lot of variability when it comes to both costs and income. As such, accounting for construction relies on the careful tracking of the expenses and profits of each project.

In addition to this variation from project-to-project, accounting for construction also needs to accommodate the long-term contracts (which can split up the collection of payments over several periods) and decentralized production (working across different job sites as opposed to a manufacturing plant).

Due to the highly customized work done by contractors, basic accounting principles must be re-evaluated and implemented in the correct way; these include:

When it comes to accounting for construction, these and other nuances need to be at the forefront of your practices to ensure that you are able to implement a system that helps instead of hinders your financial reporting and planning.

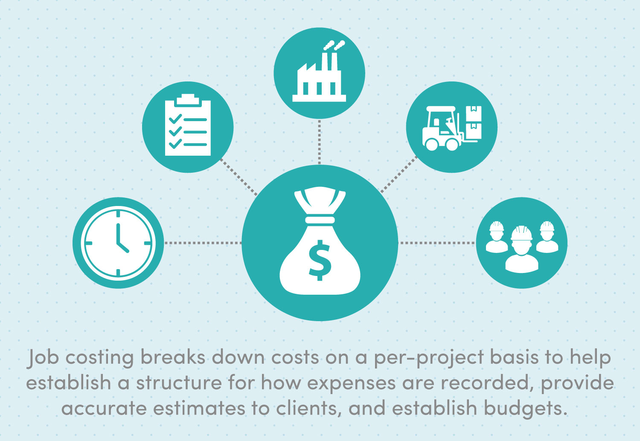

Job costing is used in addition to the general ledger to account for the costs on a per-project basis. Whereas the general ledger combines all business activities into an overview, job costing breaks down the costs of each individual project based on the various phases required. This information can then be used to:

For contractor accounting, job costing serves as a tool to provide greater stability when it comes to evaluating expenses and profits, implementing pricing and purchases, and forecasting financial aspects of the business. As such, job costing is an essential aspect of accounting for construction businesses because it facilitates well-structured and accurate financial records.

Because of the nature of construction contracts, it can be difficult to know how to account for deposits and the eventual payments that you will receive once you complete the work you’re performing for a client.

There are two traditional accounting methods that businesses can use to keep track of their income and expenses, cash-basis accounting and accrual-basis accounting:

Cash-Basis Accounting Method: Transactions are recorded when you pay for an expense and when you receive a payment for the service you have provided.

Accrual-Basis Accounting Method: Transactions are recorded at the time it is earned (when it is billed for).

Based just on that information, it may be difficult to determine which method you should use for your construction business. When it comes down to deciding between cash accounting vs. accrual accounting,

Cash-basis accounting is usually the recommended system for construction businesses. This way, transactions are only recorded when money changes hands. There are several reasons for this:

While the cash method is typically best-suited for contractor accounting, it is important to keep in mind that you will have to be more diligent about forecasting and long-term financial health when you use cash-basis accounting.

The percentage of completion method is a means of tracking revenue and expenses on a project and goes hand-in-hand with the cost-basis accounting method. Since construction contracts typically take place over long periods of time, payments may be made in periodic increments or at the time of completion on all work of the contract. In cases where payment is assured within that period, the percentage of completion method may be used to account for revenue and expenses.

The percentage of completion method is based on two factors:

On the other hand, using the completed contract method means that you will only record revenue and expenses related to a project when it is complete. However, you may find that this method can result in a greater tax burden.

Accounting standards, known as the Generally Accepted Accounting Principles (GAAP), have been established to help businesses across all industries implement effective accounting systems that are designed to comply with IRS requirements. The organization that oversees these accounting standards is the Financial Accounting Standards Board (FASB).

As part of GAAP compliance, there is a relatively new set of standards that provides guidelines for reporting revenue earned from contract work. Known as ASC 606 Revenue from Contracts with Customers, these standards provide a framework for using the percentage completed method or the contract completed method.

However, if you are a small business with under $5 million in annual profits, you are able to use the cash-basis accounting method that is not held to strict compliance with these principles. It can be beneficial to understand them and apply them as you see fit to find the best method of reporting revenue for your contracting business.

Accounting software is the modernized version of traditional bookkeeping and accounting. These systems have been developed to reduce the amount of time it takes to maintain your financial records by cutting out a lot of the frustrations that business owners face when doing their own accounting (figuring out how to categorize and record transactions, difficulty with correct calculations, and keeping track of information in one place).

There are many accounting software solutions available. Some are even customized for the construction industry—however, there is still room for error when using these programs. That’s because, at the end of the day, it’s on you to conduct your own accounting.

But what if you could have access to a streamlined, automated system and a team of financial professionals at any time? That’s where we come in.

FinancePal is a comprehensive solution for small businesses who need help with financial management. Our services can be tailored to your needs, based on your industry and the unique position your business is in.

Our team of financial professionals—from accountants to tax experts—are ready to help you take your construction business to the next level with contractor accounting services that are structured to streamline your business’s financial records and reporting.

As a contractor, you understand the importance of working with a reliable team that has training and expertise in their field, that’s what you will find when working with FinancePal. And, our services can be tailored to your needs with a la carte or comprehensive financial management services. You’ll also benefit from:

Plus, our platform is easily integrated with other tools your business uses for seamless implementation. With our team of professionals on your side, you can enjoy the peace of mind that experienced eyes are monitoring, recording, and reporting your financials, so you can focus on managing projects and growing your business.

If you are interested in comprehensive services, in addition to accounting and bookkeeping, we also offer payroll help, business formation assistance, and tax consulting and preparation services.

To save money on your small business taxes, it is important to take advantage of any tax deductions that are available to you. For construction businesses, this can include:

Even after you submit your tax return, it’s important to hold onto your records that are relevant to these deductions in case of an audit.

If you’re unsure of which business costs you can write off, our tax experts can help. Compare tax prep costs for small businesses and find out why many small business owners choose FinancePal.

As an independent contractor, you should also familiarize yourself with the specific tax obligations you are held to by visiting IRS.gov.

A successful construction business relies on proper accounting practices. Now that you have a better understanding of accounting principles as they apply to contractors, you are better equipped to make financial decisions for your business, including using FinancePal as a financial support system. Whether you just want help with your bookkeeping and accounting or want to take on comprehensive services so you can turn your focus elsewhere, you can feel confident that we serve your business’s best interests.

No matter how far you are in the weeds, our team is here to help with your bookkeeping catchup that will have your financial records in order in no time. We are here to empower you to run your business with accurate financial information that makes bidding on projects, operating your business with minimal losses, and earning a profit easier.

Jacob Dayan is a true Chicagoan, born and raised in the Windy City. After starting his career as a financial analyst in New York City, Jacob returned to Chicago and co-founded FinancePal in 2015. He graduated Magna Cum Laude from Mitchell Hamline School of Law, and is a licensed attorney in Illinois.

Jacob has crafted articles covering a variety of tax and finance topics, including resolution strategy, financial planning, and more. He has been featured in an array of publications, including Accounting Web, Yahoo, and Business2Community.

Nick Charveron is a licensed tax practitioner, Co-Founder & Partner of Community Tax, LLC. His Enrolled Agent designation is the highest tax credential offered by the U.S Department of Treasury, providing unrestricted practice rights before the IRS.

Read More

Jason Gabbard is a lawyer and the founder of JUSTLAW.

Andrew is an experienced CPA and has extensive executive leadership experience.

Contact us today to learn more about your free trial!

By entering your phone number and clicking the "Get Custom Quote" button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.

By entering your phone number and clicking the “Get Started” button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.