Due to the adverse effects of COVID-19 on many small businesses nationwide, Congress announced the Coronavirus Aid, Relief, and Economic Security Act — commonly abbreviated as the CARES Act. The $2.2 trillion economic stimulus bill ensures emergency assistance and health care response to people and small businesses facing unfortunate situations due to the 2020 coronavirus pandemic.Some of the significant clauses mentioned in the CARES Act are as follows:

● Direct payments: US nationals who are taxpayers will be eligible for a one-time direct deposit of $1,200. Married people will get $2,400 and an extra $500 for each child.

● Unemployment: The bill offers $250 million for an unemployment insurance program with extended eligibility. It also provides an additional $600 per week for four months to employees besides the state program offerings.

● Payroll taxes: The Act enables employers to pay their part of payroll taxes for 2020 until 2021 and 2022.

● Hospitals and Healthcare: The bill provides more than $140 billion to support the US’s healthcare system. $100 billion will be offered directly to the hospitals. The remaining will be allocated to provide personal and protective equipment for healthcare employees, more workforce, testing materials, and other industry-specific investments.

● 401(k) Loans: The loan limit has been raised from $50,000 to $100,000.

● RMDs: Required Minimum Distributions from IRAs and 401(k) programs (at age 72) is stopped.

● Charity: According to a new clause, there is an above-the-line cut-off for charitable grants. Also, the limit for charitable donations has been revised.

● Net Operating Losses: The Tax Cuts and Jobs Act (TCJA) net operating loss rules have been relaxed.

The Paycheck Protection Program (PPP) is a loan program designed to grant quick and direct access to small business loans with 500 or fewer workers. The PPP loan’s main focus was to support employers with payroll and operational costs during business interruptions that occurred because of the COVID-19 pandemic. Notably, borrowers could apply for PPP loan forgiveness.

The PPP has had a significant impact on small business owners struggling with their business during the coronavirus pandemic. In 2020 alone, over $500 million in loans were granted to eligible businesses.

Although the PPP offered considerable help to these businesses, the tax implications linked with these loans have left many business owners questioning what to do next. As a result of the CARES Act, the tax guidelines passed by the Small Business Administration (SBA) went through several changes.

Later the rules related to PPP and taxes were revised again in December 2020 since the Coronavirus Response and Relief Supplemental Appropriations Act (CRRSAA) passed in 2021.

The PPP loan application duration was prolonged from July to August, then December, and then March 31, 2021. Now the new extension date is May 31, 2021.

● Small businesses with 500 or fewer workers or small businesses that fulfil the SBA’s size requirements

● Restaurants or other businesses that lie within the North American Industry Classification System (NAICS) code 72, “Accommodation and Food Services,” — and employ fewer than 500 workers

● Tribal businesses

● 501(c)(19) veteran entities

● 501(c)(3) nonprofit organizations

● Sole proprietors, freelance contractors, gig economy workers, and otherwise self-employed people.

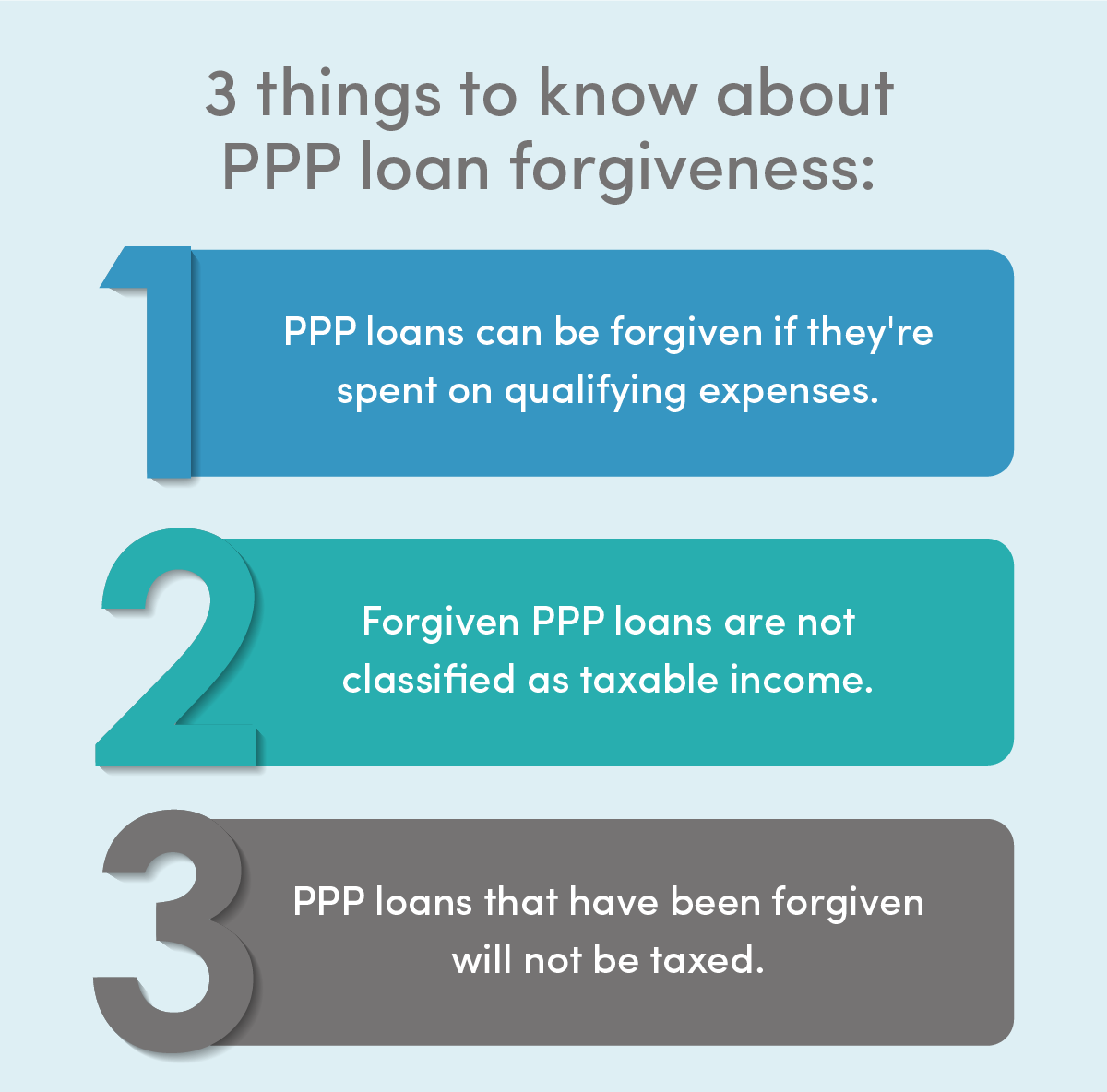

The short answer: no — if they are spent correctly.

Section 1106 (i) states, “the CARES Act provides that any amount that would be includible in the gross income of the recipient by reason of forgiveness of a PPP loan shall be excluded from gross income.”

One factor that makes the PPP appealing for businesses is the forgiveness provision. This provides loan forgiveness if the amount is used on the following expenses:

● Payroll expenditures

● Mortgage interest

● Utility bills

● Rent

● Operational expenses

● Property damage costs (because of public disruptions in 2020)

● Supplier prices

● Worker protection expenses

Businesses aren’t liable for taxes on the forgiven loan fund, according to an IRS Guide. It is expected that such loans might be forgiven. Businesses should plan strategies with their accountants for disbursing PPP loans on approved items. Notably, a small business could be eligible for a second loan if they employ fewer than 300 workers and suffered a 25 percent decrease in revenue during any quarter of 2020.

As previously mentioned, Paycheck Protection Program loan forgiveness depends on whether the PPP loan has been spent on qualifying expenses. The Treasury Department has offered several PPP Loan Forgiveness Applications, which businesses can fill and submit to the private lender who offered the loan. After passing the CRRSAA in December 2020, Congress declared that a PPP loan that has been forgiven would not be taxed — it is not categorized as taxable income.

This implies that you don’t have to pay taxes on the amount you obtain. This loan focuses on helping businesses with the cash to keep operating and paying workers. Congress specifically avoided causing tax stress for businesses receiving PPP loans.

The Paycheck Protection Program’s main objective is to keep employees on the payroll and provide cover for utilities, rent, supplier expenses, mortgage interest, and other necessary business expenditures.

The borrower can spend the loan paying any allowable costs obtained during their covered time. A financial organization can ensure that the borrower was operational as of Feb. 15, 2020. The Paycheck Protection Program has been responsible for offering forgiven loans to small-scale businesses.

At first, the loan plan had assigned $350 million in March and $320 billion in April. In December 2020, Congress allocated $284 million for new and second-time loan withdrawal for small businesses. Private lenders offer these loans, and the Small Business Administration (SBA) supports them.

Although the Small Business Administration (SBA) offered an extensive array of uses for PPP loans, they can not be used to pay business taxes. Small businesses not eligible for the PPP can still use other financing methods and carefully consider all logical sources.

The recent round of the CARES Act provides more room for small businesses to use PPP loans. Protective equipment, asset deterioration, and business software are among the latest costs covered in the PPP loan program. However, business taxes are still not included in that list. Business owners cannot pay income tax, sales tax, or any other tax with the PPP loan funds. Hence, the amount of PPP loan being used for paying business taxes will not be forgiven.

Business owners can opt for the Employee Retention Tax Credit if they fulfil the criteria. But they can not claim salaries paid with a PPP forgiven loan. To be eligible for the tax credit, a business must pay wages to workers regardless of a temporary halt due to the coronavirus lockdown or going through a 20% reduction in total receipts compared to the last year.

In 2020, many business owners failed to qualify for the Employee Retention Credit due to the credit being mutually exclusive with the Paycheck Protection Program. This is no longer the case; you can now receive an Employee Retention Credit even if you took out a PPP loan.

Eligibility requirements were also loosened; last year, businesses needed to prove a 50% reduction in income compared to the same quarter in 2019. That threshold has been lowered to a mere 20%.

The potential amount of the Employee Retention Credit has increased as well. The initial credit only covered up to 50% of qualifying wages for businesses with up to 100 active employees. The updated credit covers up to 70% of qualifying income — plus health benefits cost — for businesses with up to 500 employees.

If your business didn’t claim the ERC in 2020 due to ineligibility, you can claim the credit retroactively based on the new requirements.

If your business took out a PPP loan and you are unsure whether you can leverage it into tax savings, contact the professionals at FinancePal today! Outsourcing your accounting and bookkeeping to professionals is the most efficient and most cost-effective way to save your business money come tax time.

For many small business owners, the bookkeeping process can be a nuisance at best — and uncharted territory at worst. Most business owners started businesses because they were experts in providing a good or a service, not at balancing a book. Nevertheless, proper bookkeeping is necessary to ensure your business remains in good standing with the IRS.

The small business accounting services and small business bookkeeping services at FinancePal have helped thousands of small businesses with their financials and taxes on a convenient subscription basis. Schedule a consultation today!

Jacob Dayan is a true Chicagoan, born and raised in the Windy City. After starting his career as a financial analyst in New York City, Jacob returned to Chicago and co-founded FinancePal in 2015. He graduated Magna Cum Laude from Mitchell Hamline School of Law, and is a licensed attorney in Illinois.

Jacob has crafted articles covering a variety of tax and finance topics, including resolution strategy, financial planning, and more. He has been featured in an array of publications, including Accounting Web, Yahoo, and Business2Community.

Nick Charveron is a licensed tax practitioner, Co-Founder & Partner of Community Tax, LLC. His Enrolled Agent designation is the highest tax credential offered by the U.S Department of Treasury, providing unrestricted practice rights before the IRS.

Read More

Jason Gabbard is a lawyer and the founder of JUSTLAW.

Andrew is an experienced CPA and has extensive executive leadership experience.

Contact us today to learn more about your free trial!

By entering your phone number and clicking the "Get Custom Quote" button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.

By entering your phone number and clicking the “Get Started” button, you provide your electronic signature and consent for FinancePal to contact you with information and offers at the phone number provided using an automated system, pre-recorded messages, and/or text messages. Consent is not required as a condition of purchase. Message and data rates may apply.